What Are Closing Costs? A First-Time Homebuyer’s Guide

First-Time Homebuyer Yoshiko Oest and Russell Nomura November 25, 2024

First-Time Homebuyer Yoshiko Oest and Russell Nomura November 25, 2024

Buying a home is an exciting journey, but understanding all the expenses involved is essential. One cost that often surprises first-time homebuyers is closing costs—fees and expenses beyond the home's purchase price that are part of finalizing your purchase.

Closing costs cover a variety of services, including inspections, title insurance, and loan processing. Some fees, like appraisals and inspections, are paid early in the escrow process, while most are due just before closing. Knowing what to expect and when to pay can help you feel more prepared.

In Los Angeles, closing costs typically range from 2% to 3.5% of the home's purchase price. For example, on a $700,000 home, these costs might fall between $14,000 and $24,500, depending on factors like loan type and property location.

The amount can also vary based on how your offer is negotiated. In some cases, you may be able to ask the seller to cover part of the closing costs. Even if they won't agree to cover costs as a credit, negotiating who pays for certain expenses can impact how much you ultimately pay.

Certain loan types, such as FHA loans, often have additional requirements, like upfront mortgage insurance and escrow accounts for property taxes and homeowners insurance, which can increase costs. However, first-time homebuyer programs may offer grants ranging from $5,000 to $50,000 to help with these expenses. Some programs even allow buyers to use funds to reduce their interest rate or cover a portion of the down payment.

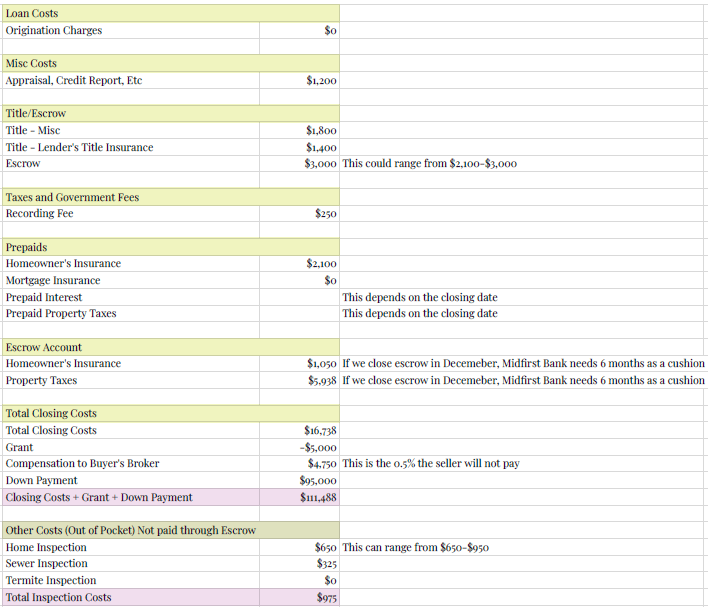

To provide a clearer picture, here's an example from clients purchasing a $950,000 home with 10% down:

The right program can significantly reduce upfront expenses, making a big difference for buyers.

Closing costs can include a variety of fees, such as:

When planning for closing costs, it's helpful to understand how and when they're paid.

Negotiation also plays a key role in determining your final closing costs. Asking the seller to cover some costs as part of your offer can significantly reduce your out-of-pocket expenses. This is where working with an experienced Realtor can make a big difference.

Closing costs may seem like a hurdle, but with preparation, they become just another step toward homeownership. If you're concerned about saving enough for these expenses, consult with an experienced Realtor. First-time homebuyer programs can make these costs more manageable, and we're here to guide you through every detail.

If you're buying a home in Los Angeles or the South Bay, we'd love to help make the process smoother. Schedule a complimentary virtual consultation using the link below—we're here to support you every step of the way.

Complimentary Virtual Consultation

Stay up to date on the latest real estate trends.

Gardena

Redondo Beach

Torrance

El Segundo

Torrance

Rancho Palos Verdes

Gardena

Torrance

Gardena

You’ve got questions and we can’t wait to answer them.